IndiView Chart of the Week: Is An Owl Actually A Canary?

Blue Owl (OWL) manages over $250 billion in private capital.

Assets under management have grown more than 250% since 2022.

So why is the stock down 44% in the past year?

Background

For most investors, Blue Owl doesn’t carry the brand recognition of JPMorgan or Apple. But in private markets, it is a significant player.

Per its 2025 investor presentation, Blue Owl manages $251 billion across:

- Private credit (54%)

- Strategic capital — primarily private equity stakes (26%)

- Real assets such as net leases and real estate (20%)

At its peak, Blue Owl carried a market capitalization of roughly $41 billion.

It is interesting for two reasons:

- Explosive growth — assets have grown at a 35% annualized rate since 2022

- A collapsing stock price — currently down more than 50% from its peak

Private Asset Management Growth

Private assets have experienced enormous growth over the past decade. Historically, these strategies were reserved for ultra-high-net-worth investors and large institutions such as foundations, endowments, pensions, and insurance companies.

More recently, the industry has expanded into the “wealth” channel — lowering access barriers for accredited investors and dramatically widening the potential capital base.

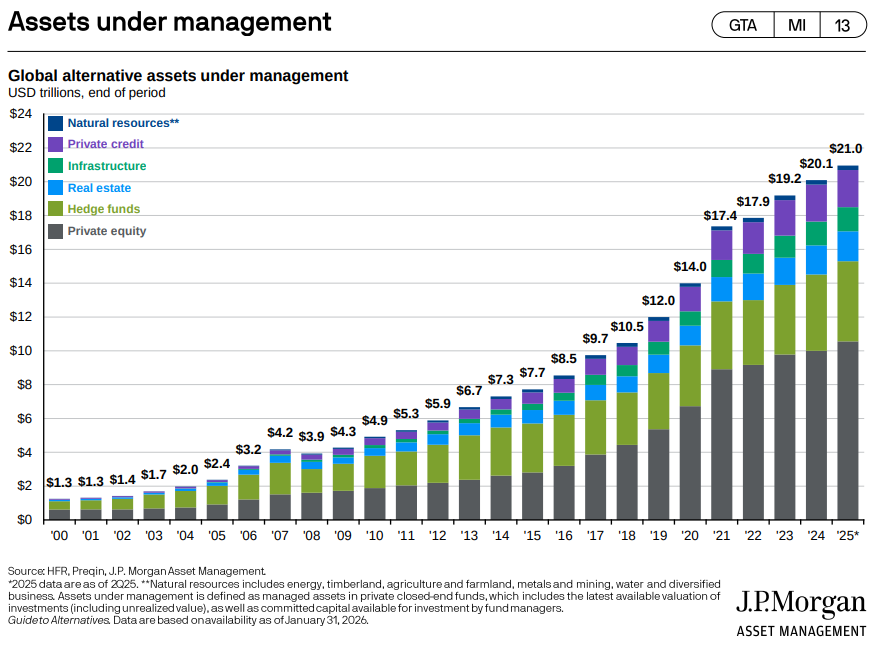

The JPMorgan chart below shows the growth across major private asset categories. The industry now represents over $21 trillion — roughly the same size as all global exchange traded funds combined.

Private markets are no longer niche.

Stock Price Doesn’t Always Follow Asset Growth

The second chart tells a very different story.

While assets under management continue to rise, public stocks of private managers have struggled.

- Blue Owl (OWL) is down 44% over the past year and more than 54% from its all-time high.

- Blackstone (BX), KKR (KKR), and Ares (ARES) are down 20–26% over the past year and 36–42% from prior highs.

It has been a brutal stretch for the sector — despite continued asset growth.

So what changed?

The Causes Of Fear

The selloff wasn’t about growth. It was about liquidity and perception.

In February, Blue Owl announced a change to its investor withdrawal policy that some perceived as a “gate” restricting redemptions from certain funds.

Shortly thereafter, the firm conducted a $1.4 billion sale of loans to provide cash to investors. Critics questioned whether the transaction reflected financial maneuvering or pressure beneath the surface.

Whether justified or not, the narrative shifted quickly.

Markets rarely isolate liquidity concerns. When one manager is questioned, contagion spreads. The selling in OWL extended to peers across the private asset space.

Growth was not the issue. Confidence was.

So, Is Blue Owl a Canary In the Coal Mine?

Short answer: yes and no.

Yes — in the sense that private asset manager stocks are highly sensitive to liquidity concerns and investor perception. When confidence wavers, declines can be swift and severe.

No — in the sense that this volatility is not new.

Over the past decade, the S&P 500 has experienced one drawdown greater than 25% (March 2020). During that same period:

- Blackstone (BX) and Ares (ARES) each experienced five drawdowns greater than 25%.

- Blue Owl (OWL) experienced two drawdowns exceeding 50%.

If you own private asset managers, you should expect drawdowns that are materially larger than those of the broader market.

That is not necessarily a signal of pending doom — but it is a feature of the business model.

These companies are publicly traded proxies for private credit sentiment, expected private market outperformance, fundraising momentum, liquidity confidence, and valuation integrity. When markets grow uneasy about any of those variables, the stocks can react aggressively.

I do not see this episode as an existential threat to the industry. I see it as an uncomfortable but common trait of private asset management equities.

The long-term trend of private asset growth remains intact. For investors willing — and able — to endure volatility, the secular growth story is still compelling.

What It Means For Investors of Publicly Traded Stocks of Private Managers

For transparency, we own Blackstone (BX) in our IndiStock portfolio and have not reduced our position during this decline.

Our thesis is straightforward:

- Private assets are likely to continue gaining share within global portfolios.

- Blackstone’s scale, diversification, and valuation position it to benefit from that trend over time.

That said, these stocks are volatile. Investor perception around liquidity, valuation, or policy changes can dramatically affect prices in the short term.

Owning them requires conviction — and tolerance for sharp swings.

What It Means for Private Asset Investors

The lesson extends beyond publicly traded manager stocks.

In public markets, investors who prefer simplicity can own broad, low-cost ETFs and effectively “buy the market.” The structure is transparent, liquidity is daily, and dispersion between managers is relatively narrow.

Private markets operate differently. In private investing, manager selection is the asset class.

There is no simple, low-cost way to passively own “the private market.” Returns depend heavily on the skill, discipline, and structure of the manager you choose. The dispersion between top and bottom performers is meaningfully wider than in public markets.

That makes the details matter — a lot.

Fee structures vary widely. Liquidity terms can differ dramatically. Valuation methodologies are not standardized. Redemption provisions may change under stress. All of these factors affect not just returns — but your ability to access your capital when you want it.

Private assets can play an important role in portfolios. But they deserve a higher hurdle rate — not blind faith.

Know what you own and why you own it.

The owl may not be a canary in the coal mine.

But it will test your tolerance for volatility.

Sources

Charts and return data: Koyfin.com as of 2/25/26

Blue Owl AUM: 2025 Investor Day Presentation (2/7/25)

This content, which contains security-related opinions and/or information, is provided for informational purposes only and should not be relied upon in any manner as professional advice, or an endorsement of any practices, products or services. There can be no guarantees or assurances that the views expressed here will be applicable for any particular facts or circumstances, and should not be relied upon in any manner. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment.

The commentary in this “post” (including any related blog, podcasts, videos, and social media) reflects the personal opinions, viewpoints, and analyses of IndiWealth employees providing such comments, and should not be regarded the views of IndiWealth LLC. or its respective affiliates or as a description of advisory services provided by IndiWealth or performance returns of any IndiWealth client.

References to any securities or digital assets, or performance data, are for illustrative purposes only and do not constitute an investment recommendation or offer to provide investment advisory services. Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. Past performance is not indicative of future results. The content speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others.

Investments in securities involve the risk of loss.