IndiView Chart of the Week: Is the Consumer Finally Saying “Uncle”?

If you follow our content here at IndiWealth, you know one of our core beliefs: the U.S. consumer drives the U.S. economy. What consumers do is shaped by a mix of job sentiment, the “wealth effect” (spending more when markets make you feel wealthier), and inflation—especially the food and energy swings that hit households directly.

Lately, we’re starting to see more signs of consumer strain. And while markets can absolutely grind higher in the near term, it becomes much harder for the economy—and ultimately the stock market—if the American consumer begins to pull back.

Sentiment Says: Not Great, Bob! (Mad Men Reference)

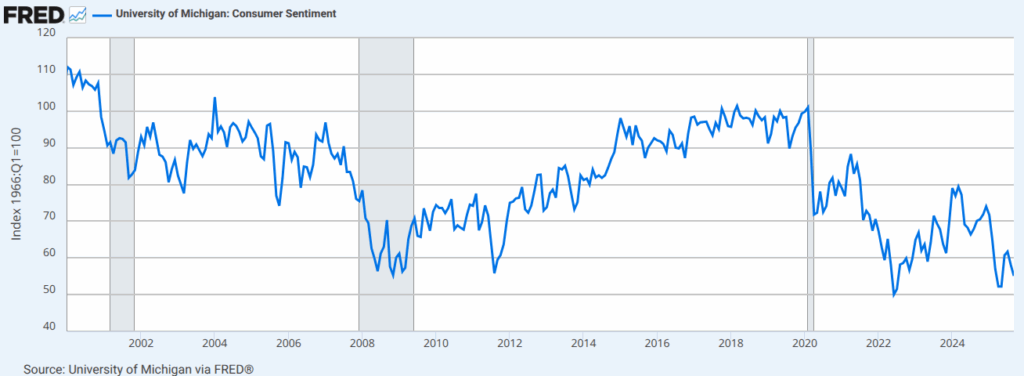

The University of Michigan’s consumer sentiment survey—those classic phone interviews that track how households feel about the economy—has been sliding for a while and is now hovering near 25-year lows. Not ideal.

But at IndiWealth, we take sentiment data with a grain (block?) of salt because:

- It hasn’t been a reliable predictor of markets or recessions.

- We prefer to assess “what consumers do, not what they say.”

So What Are Consumers Actually Doing?

We look closely at how consumer-facing companies are performing and, just as importantly, what their executives are saying about trends. Here’s what we’ve heard in just the past week:

Target: Q3 profit plunged. Persistent inflation is squeezing shoppers, and Target warned its sales slump may continue through the holiday season.

Home Depot: Cut its full-year profit forecast and missed earnings for the third straight quarter. Home improvement demand is softer, consumers are more cautious, and even storm-related spending has been lighter.

Chipotle: Lowered its annual sales forecast for the third time this year, citing pressure on dining-out budgets through early 2026.

Not exactly a booming consumer environment.

But Not Everyone Is Struggling

To avoid cherry-picking, here are two companies still showing resilience:

McDonald’s: Missed earnings overall, but U.S. same-store sales beat expectations. The CEO highlighted the company’s ability to deliver “sustainable growth” even in a challenging backdrop.

Walmart: Raised its full-year earnings and sales outlook. They acknowledge pressures on lower-income households but note that middle-income families remain relatively stable.

In short: sentiment is weak, many consumer companies are slowing, and the strength that does exist is largely in value-oriented spending.

So Why Isn’t the S&P 500 Struggling?

Because the S&P 500 simply isn’t as consumer-driven as the U.S. economy.

Consumer Staples + Consumer Discretionary together make up only 15% of the index.

And within Consumer Discretionary, the two biggest weights in the sector—Amazon (23%) and Tesla (20%)—are not traditional “consumer health” barometers. Amazon is heavily driven by tech and logistics, and Tesla trades more on EV/battery technology narratives than on U.S. household budgets.

Remove those two, and the rest of Staples + Discretionary shrink to less than 10% of the index.

For perspective:

- Amazon + Tesla = nearly 6% of the S&P

- Nvidia alone = 8%

- Microsoft + Apple = 13% combined

- Alphabet + Meta = 8%

All in, ~35% of the index is concentrated in seven mega-cap tech/AI giants whose fundamentals are driven more by cloud, chips, data, and AI trends than by weekly grocery bills or dining-out budgets.

Simply put: the S&P 500, as currently constructed, is not a proxy for the U.S. consumer.

What to Do With This

“The market isn’t the economy.” It’s a cliché because it’s true—and right now, it explains a lot.

Still, a strong, confident U.S. consumer remains essential to long-term economic health, and by extension, long-term market health. Short-term divergences between markets and consumers happen, but they don’t usually last. Over time, economic growth is the engine of market returns.

That’s why we continue to advocate for a balanced approach:

- Rebalance back to your defined risk tolerance.

- Don’t chase the handful of mega-caps doing all the lifting.

- Look for opportunity outside the “Mag 7.” Deeper diversification beyond an S&P-500-heavy allocation may be prudent right now.

If the consumer keeps weakening, markets may eventually have to acknowledge it. In the meantime, discipline and balance matter more than ever.

This content, which contains security-related opinions and/or information, is provided for informational purposes only and should not be relied upon in any manner as professional advice, or an endorsement of any practices, products or services. There can be no guarantees or assurances that the views expressed here will be applicable for any particular facts or circumstances, and should not be relied upon in any manner. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment.

The commentary in this “post” (including any related blog, podcasts, videos, and social media) reflects the personal opinions, viewpoints, and analyses of IndiWealth employees providing such comments, and should not be regarded the views of IndiWealth LLC. or its respective affiliates or as a description of advisory services provided by IndiWealth or performance returns of any IndiWealth client.

References to any securities or digital assets, or performance data, are for illustrative purposes only and do not constitute an investment recommendation or offer to provide investment advisory services. Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. Past performance is not indicative of future results. The content speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others.

Investments in securities involve the risk of loss.